Colorado Promise Guidance and Data Definitions

The following documentation is intended to assist institutions as they develop the data pull(s) associated with Colorado Promise: Expanded Two Free Years of College, or the tax credit, established in HB24-1340 and revised for technical changes in SB25-319.

Statute can be found in C.R.S 39-22-570

It is important to understand the only data elements required for reporting to CDHE are within the “Data Points for Annual Reporting” (see section below). All other topics are to help provide guidance for the data pulls. When possible, SURDS fields are referenced to help provide consistency across institutions. CDHE understands each institution’s data platforms, storage policies, and IT and data structures are unique. The data reports developed to identify eligible students will depend upon institutionally specific data structures, but the methodology and underlying criteria should be consistent across institutions.

For additional reference please review the Colorado Promise IHE FAQ for further insights.

Note: While the document is organized alphabetically, some topics are interrelated and are referenced to help provide a richer understanding.

If you have questions please reach out to the Department at ColoradoPromise@dhe.state.co.us.

Updated: 12/12/2025

- Academic vs Calendar Year for FAFSA

Guidance

The reporting and eligible semester or term(s) for a given tax year will be aligned with the calendar year, or tax year (see example below). Please note two considerations.

- The original statute aligned the tax credit to an academic year (Fall, Spring, Summer). This was changed per SB25-319 to align with the tax year to expedite students receiving the refund for out-of-pocket costs for tuition and fees.

- The first term of eligibility, Fall 2024, will be rolled into the 2025 tax year.

- Starting tax year 2026 it will only be the academic terms which took place during the calendar, or tax, year.

When considering the eligible terms for a given tax year, one must also align a given term to the correct financial aid year.

Example

Term

Tax Year

Financial Aid Year

Spring 2025

2025

2024-25

Summer 2025

2025

2024-25

Fall 2025

2025

2025-26

*Note the above table is intended to represent a typical year, but tax year 2025 will also have Fall 2024 “grandfathered” in as a one-time adjustment.See Related Topics

Terms Included

Data Definition

SURDS Enrollment File

- Report Term - enrollment period identified by the term which the data is based

- Report Term = 1 or 2 or 4

- Winter term (3) available for institutions which do not follow the traditional semester schedule, such as CSU Global

- Report Year - enrollment period identified by the calendar year on which the data are based. The tax credit spans different academic years so each term must be associated with the correct academic year.

- AGI

Guidance

Given the term-by-term eligibility of the tax credit, the AGI from the corresponding aid year FAFSA/CASFA must be used to determine eligibility. The definition of AGI is the same as used for the SURDS Financial Aid file.

Data Definition

SURDS Financial Aid File

The definition below is consistent with SURDS AGI Reporting and FISAP Family Income:

The total annual adjusted gross income (AGI) for a student and a student's parents if a student is classified as 'Dependent', or total annual adjusted gross income for a student and spouse if that student is classified as 'Independent'.

Report data for one year only. Use base year, projected year or academic year (in the case of Professional Judgment) income that was used to compute the SAI upon which aid eligibility was based.

Nonfilers will be reported on the ISIR as 1= non-filer and the Pell SAI is -1500.

Clarification: Use AGI as submitted unless manual data has been submitted.

- Credit for Failed Courses

Guidance

If a student fails one or more courses determination for their tax credit eligibility remains the same. Did they end the term with a 2.5 or better term GPA and complete at least 6 credit hours? If a student was able to fail one or more courses but still have an overall term GPA of 2.5 or better and have completed 6 credit hours then they would be eligible to receive the tax credit for all registered credits in a given term.

Data Definition

SURDS Enrollment File:

- Term GPA = ≥10

- Report Term to identify particular term

- Report Year to identify correct year

Credits completed in term:

- Course Credit Hours Passed - Number of credit hours passed for the specified student course enrollment.

- Course Credit Hours Passed ≥ 6

- Credit Hours

Guidance

In a given term of eligibility, a student must meet the following conditions related to their credit hours.

- A student is eligible if their Cumulative Credit Hours is <66 credit hours at the start of the term after subtracting exempted credits (see related topic) , which do not count towards the 65 credit hour limit.

- This should include all transfer credits (see related topic)

- Statute calls for reporting all “accumulated credits”, which follows the SURDS definition for Cumulative Credit Hours.

- Completes the term earning at least six credit hours

- Statute does not limit the number of credit hours a student can earn in a given term.

- A student may start a term below 66 credit hours but finish the term with above 66 credits, and have the full number of credits reimbursed for the given term.

- Ex: Start the term with 60 credit hours, complete 12 credits, and end the term with 72 credit hours. All 12 credit hours would be eligible for the tax credit.

- Due to the credit hour maximum a student may be eligible in a Spring term, but reach or surpass the limit (65 credit hours) and be ineligible for the remaining calendar/tax year.

See Related Topics

- Exempted Credits

- Transfer Credits

Data Definition

SURDS Enrollment File - Start of Term Credits

- Cumulative Credit Hours - the total college-level credit hours completed by the student and counted toward a degree or certificate, computed at the end of the reported term.

- This element will encompass all institutionally earned credits, transfer credits (if applicable), and precollegiate credits.

- Note - the prior term Cumulative Credit Hours may need to be used to identify the number of credits a student started a term with.

- Subtract any precollegiate exempted credits

SURDS Student Course Enrollment File - End of Term Completed Credits

- Course Credit Hours Passed - Number of credit hours passed for the specified student course enrollment.

- Course Credit Hours Passed ≥ 6

- Current Student - updated 1/16/2026

Guidance

The technical changes bill, SB25-319, noted that students who are actively enrolled as of Fall 2024 are considered eligible. Regardless if they completed high school on or after January 1, 2024. This creates a level field for students who were actively enrolled when the Colorado Promise tax credit program started in Fall 2024. If a student was an active student in Fall 2024 (student types: Continuing, New, Readmit, or Transfer) they still must meet the matriculation requirement, which states they must have matriculated to a Colorado public postsecondary institution within two years after completion of high school.

Special consideration: If a student was enrolled at a Colorado public postsecondary institution during Fall 2024 and they later transfer to another eligible institution they maintain their eligibility.

Data Definition

SURDS Enrollment File

- Registration Status - Classification divides students into categories

- Registration Status = 1 or 3 or 5

- Registration Status - Classification divides students into categories

- Data Points for Annual Reporting

Guidance

Statute requires institutions by January 31, 2026 (and each subsequent year until 2033) to report each student eligible to the Department. Institutions must report a student's Individual Taxpayer Identification Number (ITIN) or social security number (SSN), along with the amount of eligible out-of-pocket costs paid for tuition and fees. To assist Department staff with the formatting, cleaning, and matching of data, the following data points will also be required.

CDHE will utilize SURDS to annually collect data. Documents will eventually be uploaded on the CDHE Documentation page, however while Staff are implementing the SURDS modernization this process may be delayed. By September 2025 all IHE resource and guidance documents, including SURDS File documents, will be posted to Colorado Promise’s IHE Resource page.

Update 10/2/2025: CDHE Data Team has requested that student institutional ID also be collected to assist with matching across different SURDS files (Enrollment and Financial Aid) as required for data reporting to JBC and Education Committees.

Updates 12/12/2025 - the section has been updated to link SURDS documentation and to have the order of fields match the SURDS Tax Credit File order in documentation, and to confirm submission will take place via SURDS.

Note - CDHE DRP Team has confirmed the use of SURDS for submitting the tax credit file. If there there is a unexpected technical issue, CDHE has a contingency system, ShareFile, to assure a secure data transmission process.

- Record Type

- Institution Code

- Student ID INST

- Report Term

- Report Year

- Tax Payer ID Type

- First Name

- Last Name

- Tax Credit (by Term)

- Fall (2024) Term - pick up for 1st year only

- Spring Term Amount

- Summer Term Amount

- Fall Term Amount

Data Definition

- See SURDS Tax Credit File documentation on the Colorado Promise IHE Resource webpage

- Degree/Credential Seeking

Guidance

A student must be enrolled as a degree or credential seeking undergraduate student.

While statute does not clearly articulate, students must be working on their first degree or, in the case of certificates, a student may work on multiple certificates within the credit limitations allowed by statute. This is based on the term eligibility of a student having completed <66 credit hours at the start of a term. Students who have already completed a BA will have completed at least 120 credit hours if they have already earned a bachelors.

Data Definition

The degree-seeking undergraduate criterion is based on the Student Level field and requires a student to be reported with one of codes 11, 12, 13, 14, or 15, with 12-15 acknowledging college credit earned for work done during high school through concurrent enrollment and/or AP/IB.

SURDS Enrollment File

- Degree Level = 11, 12, 13, 21

- Certificates = 01, 02,

- 03 (allowed if a student enters with precollegiate credits)

- Certificates = 01, 02,

- Degree Level = 11, 12, 13, 21

- Electronic Communication

Guidance

Per technical changes: C.R.S. 39-22-570 (4)(b) Institutions are allowed to provide students with an electronic statement and are not required to provide information in a physical form.

CDHE is partnering with the Colorado Department of Revenue (DOR) to develop a template for institutions to use. At this time, DOR will not require a separate tax form for the tax credit, so the institutional communication will suffice. Visit the Colorado Promise website for IHE and Educational Partner Resources for a template of the notification communication. Institutions should place the template on an official institutional letterhead, or other designated document, to aid DOR in fraud prevention.

Data Definition

No definition - guidance only

- Exempted Credits

Guidance

Statute C.R.S. 39-22-570 (2)(e)(I) specifies that precollegiate credits earned prior to postsecondary enrollment, such as AP, IB, military, and concurrent enrollment, will not count towards the 65 credit hour maximum for the program.

AP, IB, and military credits are specified on a student's transcript, and can be subtracted or dropped from the cumulative credit hours.

Students who earn college credits from participation in the ASCENT program should also have those credits subtracted as those credits were earned prior to their official high school graduation.

Institutional feedback identified several challenges with identifying certain types of precollegiate credits, specifically concurrent enrollment earned at another institution.

Options for determining other pre-enrollment credits (Concurrent, ASCENT):

- Utilizing the Year of HS Grad (SURDS Enrollment file) and first known term of postsecondary enrollment to identify any credits earned prior to the first term of postsecondary enrollment.

- Determine approximate term of HS Graduation

- Identify credits earned at time of HS graduation or before*

*For institutions which do not capture the term transfer credits were earned, please see option #2.

- Use the COF Response File* sent from CollegeAssist and use the “Lifetime Concurrent Hours” data element to identify the total number of credits earned from all institutions. This field is available at the student level and can be subtracted from cumulative credit hours.

- C.R.S. 23-18-202 (5)(c)(III) identifies credits completed while a student was enrolled in high school which DO NOT count towards the COF lifetime limitation. These credits, listed below, represent the same precollegiate credits the tax credit (C.R.S. 39-22-570 (2)(e)(I) or 1340) identifies as being exempted from the 65 credit hour limit.

- Concurrent Enrollment

- ASCENT

- TREP program

- Prior learning assessment

*This option is only available for students who have applied for the Colorado Opportunity Fund (COF), while COF is not a required component of the Colorado Promise tax credit program students are highly encouraged to apply.

See Related Topics

- Credit Hours

- Transfer Credits

- High School Graduation - if a student earned a GED

Data Definition

If using Option #1 - credits earned prior to start of higher education

SURDS Enrollment File

- Year of HS Grad - four digit year in which the student graduated from high school. When developing the data pull it is acceptable to assume the graduation term is the spring semester.

- Cumulative Credit Hours - the total college-level credit hours completed by the student and counted toward a degree or certificate, computed at the end of the reported term.

- This element will encompass all institutionally earned credits, transfer credits (if applicable), and precollegiate credits.

- Note - the prior term Cumulative Credit Hours may need to be used to identify the number of credits a student started a term with.

- Subtract any precollegiate exempted credits

If using Option #2 - Lifetime Concurrent Hours

- The data field will be included in the latest “Response File” received from CollegeAssist. Storage and processing of the “Response File” is specific to each institution. It is recommended that you contact your institutional IR or Office of Financial Aid to determine the primary contact.

- Subtract the lifetime concurrent hours along with any IB, AP, or military credits from the cumulative credit hours.

- FAFSA Completion

Guidance

A completed FAFSA/CASFA is one that has been thoroughly filled out, submitted, signed and consent given by all required contributors, and processed without any issues. An official SAI must be calculated to be considered complete. If the student is selected for verification or conflicting information is identified by the IHE, all necessary documentation must be submitted to the IHE and processed before the FAFSA/CASFA is complete.

Data Definition

No definition - guidance only

- Fall 2024 High School Graduation Date Exception - Edited 1/16/2026 (examples provided)

Guidance

C.R.S. 39-22-570(2)(c)(I) “Completed high school graduation or an equivalent on or after January 1, 2024, or is currently enrolled as of fall 2024”. This section of statute provides an exemption for the January 1, 2024 or later high school completion requirement for students who were currently enrolled during the Fall 2024 term. Any student who was enrolled during the Fall 2024 term at a Colorado public postsecondary institution regardless of student type (readmit, current, transfer, or first-time) automatically met the high school date completion date requirement. Students enrolled in fall 2024 do not need to have graduated or completed high school on or after January 1, 2024.

While students enrolled during fall 2024 term meet the high school graduation date requirement, they still must meet the matriculation requirement. This means that a student enrolled in fall 2024 may be eligible as long as they originally matriculated to a Colorado public postsecondary institution within two years of graduating high school; this could have occurred at any time in the past. However, students enrolled in fall 2024 who took 3 or more years off between high school and their initial postsecondary enrollment are not eligible.

Examples:

Qualifying Student: graduates high school in spring 2017 first enrolls at a Colorado public postsecondary institution fall 2018.

NOT Qualifying Student: graduates high school spring 2017 first enrolls at a Colorado public postsecondary institution fall 2021.

As with other cases where it is challenging for institutions to determine a students first term of postsecondary enrollment, the Department directs institutions to utilize a process and system which best meets their internal capacity for collecting the required information.

See Related Topics

- High School Graduation

- Matriculation

- Transfer Students

Data Definition

No definition - guidance only

Special Note: Several institutions have noted they are developing internal flags to identify students who have met the high school graduation date and matriculation requirements to aid in more efficient data pulls.

- Full-Time vs Part-Time Enrollment

Guidance

Enrollment intensity does not apply when determining eligibility for the tax credit. Rather the number of credits earned at the end of a semester or term determines eligibility. A student must complete at least six semester credit hours for said term to be considered eligible for the tax credit.

Data Definition

No definition - guidance only

- GPA - updated 12/12/2025

Guidance

The cumulative GPA for a student does not influence eligibility for the tax credit. The end of term GPA must minimally be 2.5 after final grades have been submitted. The term GPA is based on available data pulled after the January 15th data change deadline, which occurs the January following the tax year (Ex for Spring 2025 data the data deadline or freeze date is January 15, 2026). Grade or data changes which occur after the January 15th deadline, while permissible by institutional policies, does not impact

Eligibility for the tax credit is not based on a student maintaining SAP. A student may fall below SAP, but have a term in which they complete six or more credits with a GPA of 2.5 or better. In this manner, the tax credit can help to provide support and resources for a student to continue with their education while other sources of financial aid are not available.

Data Definition

SURDS Enrollment File:

- Term GPA - GPA recorded in a students’ transcript for the current term, computed at the end of the reported term

- Term GPA = ≥10

- Report Term - enrollment period identified by the term which the data is based

- Report Term = 1 or 2 or 4

- Winter term (3) available for institutions which do not follow the traditional semester schedule, such as CSU Global

- Report Year - enrollment period identified by the calendar year on which the data are based. The tax credit spans different academic years so each term must be associated with the correct academic year.

- Term GPA - GPA recorded in a students’ transcript for the current term, computed at the end of the reported term

- High School Graduation

Guidance

To be considered eligible for the tax credit a student must have graduated or completed high school or equivalent on or after January 1, 2024, or have been currently enrolled at an institution of postsecondary education during Fall 2024.

If a student completed a GED or has a non-reported year of high school completion then they must report the date of completion to the institution to be considered for program eligibility. The GED Score field (SURDS Undergraduate Applicant File) does not capture the date when the equivalency test was completed.

While most institutions will capture this information as part of the application and transcript process, the Department directs institutions to utilize a process and system which best meets their internal capacity for collecting the required information.

Institutions are not expected to report completion dates as part of the Promise Reporting.

See Related Topics

- Matriculation

Data Definition

SURDS Enrollment File

- Year of HS Grad - four-digit year in which the student graduated from high school

- Year HS Grad ≥ 2024

- Report Term - the enrollment period identified by the term on which the data are based

- Report Term - to identify first term, or minimum term, enrolled as a non-high school or special Registration Status

- Registration Status - classification divides students into three major categories - first time, transfer, and continuing/readmit.

- Registration Status = 1 (first-time) for new, first-time students

- In-State Tuition

Guidance

As defined in CRS 23-7-102(5):

"In-state student" means a student who has been domiciled in Colorado for one year or more immediately preceding registration at any institution of higher education in Colorado for any term or session for which domiciliary classification is claimed, but attendance at an institution of higher education, public or private, within the state of Colorado shall not alone be sufficient to qualify for domicile in Colorado. "In-state student" includes a member of the armed forces of the United States or his dependents who qualify under section 23-7-103 (1)(c).

For more details regarding Colorado Residency Status please see the CDHE site for the entire Title 23 statute.

Data Definition

SURDS Financial Aid File

- Tuition Classification - Classification of student for purposes of tuition assessment

- Tuition Classification = 1

- Tuition Classification - Classification of student for purposes of tuition assessment

- Matriculation - updated 1/16/2026

Guidance

A student must matriculate from high school to a Colorado public postsecondary education within two academic years. This should be determined by comparing their high school graduation/completion date with their initial term of registration.

SB25-319 amends C.R.S. 39-22-570 (2)(c)(I.5) to clarify that a student must matriculate from high school to a Colorado public postsecondary education within two years of high school graduation or equivalent.

Students, particularly transfer students, should submit high school graduation dates as well as transcripts which show their first term of postsecondary enrollment at a Colorado public postsecondary institution. The Department has heard from institutions that transfer students create challenges given their current data structures and practices, and directs institutions to utilize a process and system which best meets their internal capacity for collecting and determining that transfer students have met the matriculation requirement.

See Related Topics

- High School Graduation

- Transfer Students

Data Definition

SURDS Enrollment File

New, First-Time Students:

- Year of HS Grad - four-digit year in which the student graduated from high school

- Year HS Grad ≥ 2024

- Report Term - the enrollment period identified by the term on which the data are based

- Report Term - to identify first term, or minimum term, enrolled as a non-high school or special Registration Status

- Registration Status - classification divides students into three major categories - first time, transfer, and continuing/readmit.

- Registration Status = 1 (first-time) for new, first-time students

- Post-Term Changes

Guidance

Amend section 39-22-570 Add (3)(C) WITH REGARD TO WHETHER A PERSON IS AN ELIGIBLE STUDENT, OR A SEMESTER OR TERM IS A QUALIFYING SEMESTER OR TERM, THE COLORADO PUBLIC INSTITUTION OF HIGHER EDUCATION SHALL TAKE INTO ACCOUNT THE FACTS AND CIRCUMSTANCES DETERMINED ON OR BEFORE JANUARY 15th FOLLOWING THE NEW TAX YEAR AND SHALL DISREGARD ANY CHANGE IN FACTS OR CIRCUMSTANCES OCCURRING AFTER THAT TIME.

All data changes, such as grade changes, must be completed by January 15th in order for data to be utilized in determining eligibility for the Colorado Promise tax credit. This does not supersede institutional policies regarding timelines for grade changes, tuition appeals, etc., but only applies for determining eligibility for the tax credit.

Data Definition

No definition - guidance only

- Professional Judgements

Guidance

Professional Judgements (PJs) are instances when institutions provide a review of additional materials which impact a student’s financial status. Institutions are allowed to submit changes which impact a student’s financial aid packaging, and potentially their eligibility for the tax credit.

PJs can proceed and should follow US Federal Aid guidelines as well as individual institutional policies and procedures. For a PJ to be applicable it must be completed and all data finalized by January 15th, as that is the deadline for all data changes as laid out in statute (see Post-Term Changes).

Data Definitions

No definition - guidance only

- Readmit Students

Guidance

SB25-319 amends C.R.S. 39-22-570 (2)(c)(I) to clarify that readmit students who graduated high school prior to January 1, 2024 are not eligible for the Colorado Promise tax credit. The amended language specifies that a student must matriculate from high school to a Colorado public postsecondary education within two years of high school graduation or equivalent ON OR AFTER JANUARY 1, 2024, OR IS (was) CURRENTLY ENROLLED AS OF FALL 2024*.

The Department further clarifies that “currently enrolled” refers to enrollment at a Colorado public postsecondary institution of higher education.

*If a student was a readmit student in the Fall of 2024 they should be included as an eligible student, regardless of the matriculation status.

In future terms, readmit students do present a technical challenge. Similar to a transfer students, institutions will need to determine if a student who is being readmitted originally met the matriculation requirement (i.e. they completed high school after January 1, 2024 and enrolled at a Colorado public postsecondary education within two academic years). Statute does not require continuous enrollment, and does not penalize students for stopping out. If a student stops out and returns to college they will be eligible for the tax credit, if they meet all eligibility requirements.

Institutions need to capture students’ year of high school graduation, or equivalent. Please see High School Graduation for further information.

See Related Topics

- High School Graduation

- Matriculation

- Transfer Students

Data Definition

No definition - guidance only

- Student Identification - updated 12/12/2025

Guidance

In order to file a tax return an individual must submit either, 1) SSN, OR 2) ITIN. CDHE highly encourages institutions to confirm individuals SSN/ITIN on file in order to successfully have a tax credit processed by the Colorado Department of Revenue.

Update 12/12/2025 - As previously shared, the Department is also asking institutions to report a students institutional ID number. This number will be used to help the Department connect reported data to other SURDS files for required reporting. Institutions will also utilize the student institutional ID when developing the Tax Certificate number.

See Related Topics

- Data Points for Annual Reporting

- Tax Certificate Number

Data Definition

SURDS Enrollment File

- Student ID Field Definition - a number that uniquely identifies a student at an institution, SURDS notes that when possible this should be a nine digit social security number

- Student ID Type - indicator to classify the Student ID number to be either a SSN or institutional assigned ID number

- Student ID Type ≠ 1

- Tax Certificate Number - new 12/12/2025

Guidance

The Department of Revenue (DOR) requested that a unique tax certificate number be generated to assist with reconciliation, auditing, and fraud mitigation. The number is unique for each student for each tax year, and is developed by combining fields already being reported on the SURDS Tax Credit file. The tax certificate number should also be included on the notification message sent to eligible students.

The tax certificate number should be the same across all eligible terms in a given tax year.

The number combines the following fields into a single number:

- Tax Year: 4 digit number (ex 2025)

- Institutional code: 4 digit number (ex 1234)

- Student ID INST: upto 9 digit alphanumeric (ex 987654321)

- EXAMPLE Tax Certificate Number: 20251234987654321

Data Definition

- See SURDS Tax Credit Field Definitions

- See SURDS Tax Credit File Layout

- Terms Included

Guidance

For the initial year of the tax credit, 2025, the following terms will be considered.

- Fall 2024 (rolled into 2025)

- Spring 2025

- Summer 2025

- Fall 2025

Starting January 2026 eligible terms will follow the calendar or tax year with the following eligible terms.

- Spring

- Summer

- Fall

See Related Topics

- Academic vs Calendar Year for FAFSA

Data Definition

SURDS Enrollment File

- Report Term - enrollment period identified by the term which the data is based

- Report Term = 1 or 2 or 4

- Winter term (3) available for institutions which do not follow the traditional semester schedule, such as CSU Global

- Report Year - enrollment period identified by the calendar year on which the data are based. The tax credit spans different academic years so each term must be associated with the correct academic year.

- Third Party Payments

Guidance

Third Party payments are considered “Other Forms of Assistance” (OFA) and should follow the guidelines provided in the 2025-2026 Federal Student Aid Handbook (see chapter 3 Packaging Aid). The federal guidance directs that funds that can be “reasonably anticipated at the time you award aid to the student, whether the assistance is awarded by the school or by an individual or organization outside the school” should be considered OFA. The Department recommends following institutional policies and practices for determining and handling OFA for consistency. If the source is overseen or distributed by the institution, then the Department recommends including them in the OFA “bucket” used to determine the eligible amount for tax credit.

If an institution has outstanding questions regarding funds that fall into the OFA category (20 U.S.C.A § 1087vv(i) defines other financial assistance), it is encouraged to consult legal counsel.

Finally, unless mandated by institutional policy, if payments originated from a family member (parent, grandparent, etc.) those payments should not be considered as OFA and should NOT be included when determining amounts eligible for the tax credit, as those funds are not normally included in standard reporting, such as SURDS Financial Aid File.

Data Definition

No definition - guidance only

- Transfer Credits

Guidance

All transfer credits which are counted towards a student's reported Cumulative Credit Hours (SURDS Enrollment file) should be included in calculations in determining eligibility. However, credits earned prior to a student’s high school graduation/completion should be considered precollegiate Exempted Credits (see above section) and subtracted from the cumulative credit hour total.

See related topics

- Credit Hours

- Exempted Credits

Data Definition

SURDS Enrollment File

- Cumulative Credit Hours - the total college-level credit hours completed by the student and counted toward a degree or certificate, computed at the end of the reported term.

- This element will encompass all institutionally earned credits, transfer credits (if applicable), and precollegiate credits.

- Precollegiate credits, or exempted credits, should be backed out of the total Cumulative Credit Hours. These credits include AP, IB, military, concurrent, etc.

- Transfer Students

Guidance

Transfer students can be eligible for Colorado Promise’s tax credit. Students will need to provide the accepting institution with the following documentation so that their eligibility can be determined:

- Year of high school completion (see High School Graduation)

- Transcripts (see Transfer Credits) which demonstrate they matriculated to a Colorado public postsecondary institution within two years of high school completion, unless they were enrolled at a Colorado public institution during Fall 2024.

Accepting institutions will need to determine the first term of postsecondary enrollment at a Colorado public postsecondary institution after high school completion.

See related topics

- Credit Hours

- Exempted Credits

- High School Graduation

- Matriculation

- Transfer Credits

Data Definition

No definition - guidance only

- Tuition and Fees

Guidance

C.R.S. 39-22-570 (2)(g) defines “tuition and fees” based on IRS Code Section 25A (f)(1). The section addresses qualified tuition and fees required for the enrollment or attendance of the student at the institution, and does not reference or incorporate additional language to include books, supplies, and equipment.

The tax credit, created through Colorado Promise, covers the tuition and fees paid by a student. The tax credit does not cover broader educational costs, such as books, supplies, and equipment, which may be covered by federal tax credits.

For purposes of the Colorado Promise tax credit, tuition and fees must be calculated on a term-by-term basis, to account for term-based academic eligibility requirements, such as end of term GPA and minimum 6 credit hours completed.

For a given term, the amount eligible for the tax credit is the out-of-pocket costs for tuition and fees a student paid. Out-of-Pocket tuition and fees means the amount remaining after all forms of “free” aid (grants, scholarships, and miscellaneous awards such as COF) were applied.

Excluded Sources:

- Loans, both federal and private, should not be included in the determination of tax credit amount.

- Federal and Colorado Work Study

Data Definition

SURDS Financial Aid File -

- Determining all “free” aid

- Federal Pell - dollar amount of a Federal Pell Grant paid to a student

- Federal SEOG - dollar amount of the Federal Supplemental Education Opportunity Grant paid to the student

- Other Federal Grants - amount of aid received from federal sources excluding Title IV

- Colorado Student Grant - paid amount of need based Colorado Student Grant Award

- Colorado Categorical Grant - disbursed dollar amount of a Colorado Categorical Grant award

- Institutional Need Based Awards - award that was paid to the student from institutional funds where financial need is either the only component of the primary component used to determine the recipient

- Institutional Merit Based Funds - award that was paid to the student from institution controlled funds

- Other Scholarship - dollar amount paid to a student from a source other than Federal, State, or institutional foundation funds and for whom the institution does not select the recipient

- GearUp Scholarship - scholarship for participants in the Colorado GearUp program

- Colorado Teach Scholarship - dollar amount of the Colorado Teach scholarship

- Federal Teach Scholarship - dollar amount of the Federal Teach Grant

- Colorado CTE Grant - dollar amount of the CTE Grant award paid to a student

- Colorado COSI - state dollar amounts awarded to a student from a Colorado Opportunity Scholarship Initiative (COSI)

- Colorado FosterEd - state dollar amount paid to the student receiving the FosterEd Award

- Colorado EmpowerEd - state dollar amount paid to the student receiving the EmpowerEd Award

NOTE: C.R.S. 39-22-570(6)(d)(II), as amended in SB25-319, requires institutions to annually report student level tuition and fees. This field will be added to the SURDS Financial Aid File, however given the SURDS recovery and modernization work the timeline for the additional field has not been established. CDHE will inform institutions as the fields are developed and advance notice before reporting is due.

- Undergraduate

Guidance

A student must be classified as an undergraduate student working on their first degree. A student who has already completed a BA should not be considered eligible since they have already completed more than 65 credit hours.

Data Definition

SURDS Enrollment File

- Student Level

- Degree Seeking = 11, 12, 13, 14, 15, or 16

- 13, 14 - allowed if a student enters with credits completed

- Student Level

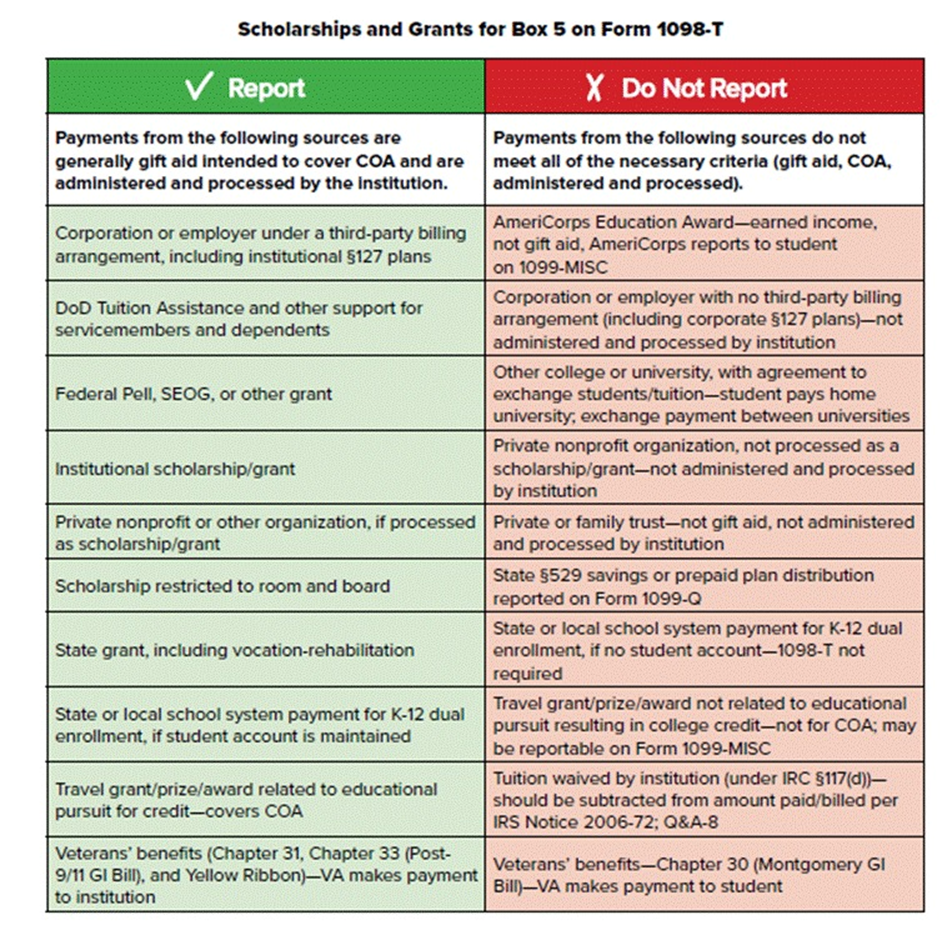

- VA Benefits

Guidance

With regards to VA benefits, utlization of the 1098-T guidance provides a consistent process to aid Offices of Financial Aid and Bursars in correctly allocating funds which should be accounted for when determining the amount of funds a student is eligible to receive. Please see the bottom row to aid in the differentiation of VA benefits.

Data Definition

No definition - guidance only